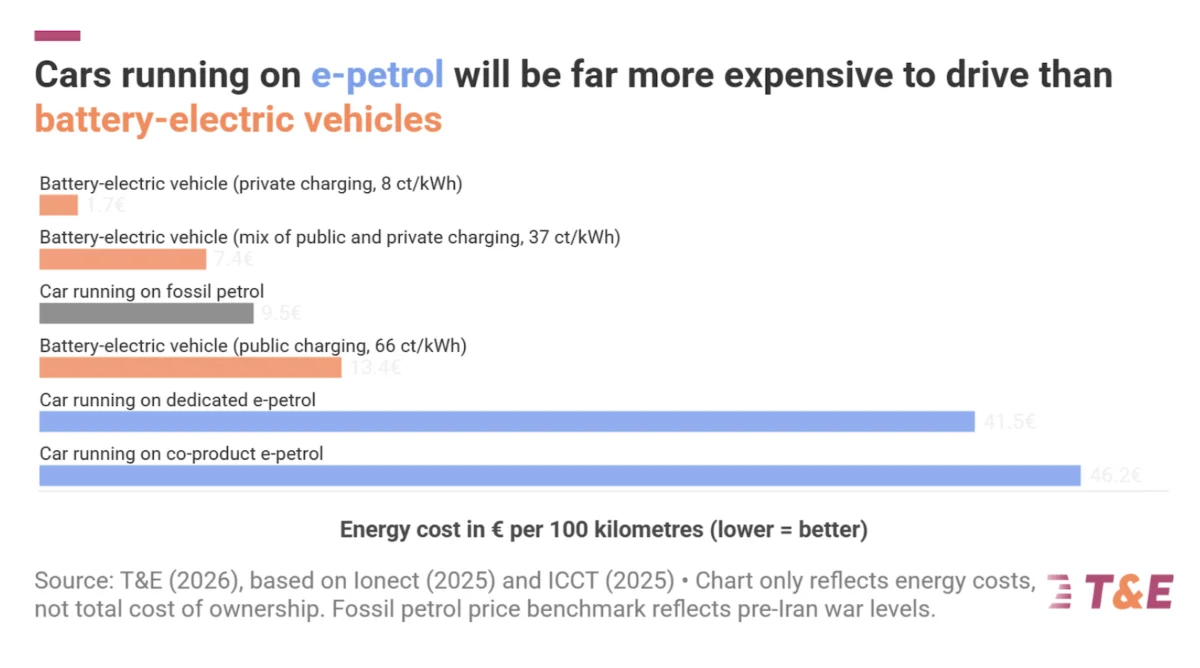

The debate over the future of the internal combustion engine has reached a critical juncture as new data suggests that synthetic "e-petrol" will remain a prohibitively expensive alternative for the average consumer. A comprehensive independent study commissioned by the environmental federation Transport & Environment (T&E) and conducted by the consultancy firm Ionect has revealed that the production costs and market prices of e-fuels are likely to far exceed those of both traditional fossil fuels and electric vehicle (EV) charging. The study, which assesses the technical feasibility and near-term economic outlook of e-petrol, concludes that by 2030, the cost of producing a single liter of e-petrol could hover around €4. When accounting for distribution, taxes, and retail margins, this figure is projected to rise to approximately €7 per liter at the pump.

This price point represents a stark contrast to current fossil fuel prices, which typically remain below €2 per liter in most European markets. The findings challenge the narrative promoted by some automotive industry stakeholders and political factions who suggest that e-fuels could serve as a "drop-in" carbon-neutral solution for existing passenger car fleets. Instead, the data suggests that e-petrol would be a luxury product, largely unaffordable for the general public, especially as battery-electric mobility continues to benefit from economies of scale and decreasing operational costs.

Technical and Economic Hurdles in E-fuel Production

E-fuels, or synthetic fuels, are produced using a Power-to-Liquid (PtL) process. This involves capturing carbon dioxide (CO2) from the atmosphere or industrial sources and combining it with hydrogen produced through the electrolysis of water using renewable electricity. While chemically identical to conventional petrol, the energy intensity of this process is significantly higher than that of direct electrification.

The Ionect study highlights that the high cost of e-petrol is fundamentally linked to the inefficiency of the energy conversion chain. To power a vehicle with e-fuels, renewable energy must first be converted into hydrogen, then synthesized into a liquid fuel, transported, and finally burned in an internal combustion engine (ICE). At each stage, significant energy losses occur. In contrast, an electric vehicle uses renewable electricity directly to charge a battery, which then powers a motor with high efficiency. Research suggests that an EV can travel five to six times further than an e-fuel-powered car using the same amount of initial renewable energy.

Beyond the energy penalty, the capital expenditure required for carbon capture and electrolysis infrastructure remains high. The study indicates that even with optimistic projections for technological advancement by 2030, the "green premium" on synthetic petrol will remain substantial. This economic reality places e-fuels in a difficult position within the consumer market, where the total cost of ownership is a primary driver for vehicle adoption.

The Aviation Co-product Narrative

One of the primary arguments in favor of e-petrol for cars has been the "co-product" theory. Proponents suggest that as the aviation industry scales up the production of e-kerosene (synthetic jet fuel) to meet sustainable aviation fuel (SAF) mandates, other fuel fractions like e-petrol will be produced as unavoidable by-products. The logic follows that these co-products could be sold cheaply to the road transport sector.

However, the Ionect study explicitly deconstructs this narrative. The research concludes that producing e-petrol as a derivative of aviation fuel production would actually be more expensive than dedicated e-petrol production. Furthermore, the volume of these co-products is expected to be negligible. T&E estimates that any potential e-petrol volume generated as a byproduct of aviation fuel would account for less than 3% of the total fossil petrol consumed by European cars in 2035.

Crucially, the study also finds that chemical engineering processes allow for the avoidance of these co-products entirely. With a modest additional production cost of approximately 10%, refineries can optimize their output to focus solely on aviation or maritime fuels, which are harder to electrify than passenger cars. Alternatively, any unavoidable light fractions could be redirected to the chemicals sector for use in plastics and other industrial applications, rather than being burned in car engines.

Environmental Impact and Air Quality Concerns

The push for e-fuels is often framed as a way to maintain the utility of the internal combustion engine while achieving climate neutrality. While e-fuels can be carbon-neutral if the CO2 used in production is captured from the air and the electricity used is 100% renewable, they do not address the issue of tailpipe air pollution.

Burning e-petrol in a traditional engine still results in the emission of nitrogen oxides (NOx), carbon monoxide, and particulate matter. Recent laboratory tests have shown that cars powered by e-petrol emit levels of air pollutants similar to those powered by fossil petrol. For urban centers struggling with air quality standards, the continued use of combustion engines—regardless of the fuel source—represents a public health challenge that battery-electric vehicles, which have zero tailpipe emissions, effectively solve.

Chronology of the European E-fuel Debate

The integration of e-fuels into European policy has been a contentious journey, marked by intense lobbying and geopolitical maneuvering.

In July 2021, the European Commission introduced the "Fit for 55" package, which included a proposal to effectively ban the sale of new internal combustion engine vehicles by 2035 by setting a 100% CO2 reduction target. This move was intended to provide a clear investment signal for the transition to electric vehicles.

By 2022, the European Parliament and Member States reached a preliminary agreement on this target. However, in early 2023, Germany—under pressure from its domestic automotive lobby and the junior partner in its governing coalition, the FDP—staged a last-minute intervention. Germany demanded a legal loophole that would allow the sale of new ICE vehicles after 2035, provided they run exclusively on CO2-neutral e-fuels.

This led to a compromise where the European Commission agreed to create a new category for "e-fuel only" vehicles. Since then, the debate has shifted to how these vehicles will be regulated and whether a "fuel credits" mechanism should be introduced. Such a mechanism would allow carmakers to count the use of e-fuels in the general fuel mix toward their fleet CO2 targets, a move that environmental groups like T&E argue would undermine the integrity of the 2035 phase-out.

Analysis of the Proposed Fuel Credits Mechanism

The European Commission’s consideration of a compensation or "credits" mechanism for fuels has drawn sharp criticism from policy analysts. Under such a system, car manufacturers could be rewarded with lower CO2 targets if fuel suppliers place a certain amount of biofuels or e-fuels on the market.

T&E strongly recommends that co-legislators reject this mechanism. The organization argues that it would artificially inflate the cost of decarbonization for both the industry and drivers. By allowing manufacturers to continue producing combustion engines, the mechanism risks diverting investment away from the EV supply chain and battery technology, where Europe is currently competing with dominant players in China and the United States.

Furthermore, a credit system creates a complex regulatory environment that is difficult to monitor. Ensuring that a vehicle is "exclusively" using e-fuel would require sophisticated sensor technology and refueling interlocks, adding further cost and complexity to the vehicle’s design.

Broader Industrial and Economic Implications

The findings of the Ionect study have significant implications for the European automotive industry’s global competitiveness. As China rapidly scales its EV production and charging infrastructure, European manufacturers risk falling behind if they remain tethered to internal combustion technology through the high-cost "life support" of e-fuels.

From a consumer perspective, the transition to electric mobility is increasingly viewed as an economic necessity. While the upfront cost of EVs has historically been higher, the gap is closing, and the operational costs—including fuel and maintenance—are significantly lower than those of ICE vehicles. Forcing a segment of the market toward e-petrol at €7 per liter would likely result in a "mobility divide," where only the wealthiest drivers can afford to operate new combustion-engine cars, while the majority of the population transitions to more cost-effective electric alternatives.

The industrial argument for e-fuels is often centered on preserving the existing engine manufacturing workforce. However, economists argue that this may result in "stranded assets"—factories and skills dedicated to a technology that the market can no longer support due to the high cost of the fuel required to run it. A cleaner break toward electrification, supported by robust retraining programs, is seen by many as a more sustainable path for the European labor market.

Conclusion and Future Outlook

The Ionect study reinforces the growing consensus among energy experts that e-fuels are not a viable "Plan B" for passenger road transport. The projected price of €7 per liter at the pump makes e-petrol an unrealistic solution for mass-market decarbonization. Instead, the role of e-fuels is likely to be confined to sectors where direct electrification is technically unfeasible, such as long-haul aviation and maritime shipping.

As the European Commission and Member States finalize the technical details of the post-2035 regulations, the pressure is mounting to prioritize efficiency and affordability. The evidence suggests that a clear, unwavering commitment to battery-electric vehicles remains the most effective way to meet climate goals while ensuring that mobility remains accessible to the average European citizen. T&E’s call to delete the proposed fuel credits mechanism serves as a warning that regulatory diversions could delay the inevitable technological shift, ultimately costing both the industry and the consumer more in the long run.

The next few years will be decisive for the European automotive landscape. As infrastructure expands and battery prices continue their downward trajectory, the economic case for e-petrol in cars appears increasingly fragile. For policymakers, the challenge lies in resisting short-term political pressures in favor of a long-term strategy that aligns with both environmental science and economic reality.

{kind=link}

Leave a Reply