The United States electric vehicle (EV) sector experienced a notable contraction during the first quarter of 2026, marking a significant departure from the rapid growth trajectories observed over the previous five years. According to the latest registration and sales data, the EV share of the total U.S. automotive market fell to 5.9% in Q1 2026. This figure represents a sharp decline from the 7.6% market share recorded in the first quarter of 2025 and a substantial retreat from the industry’s historic peak of 10.6% achieved in the third quarter of 2025. This downturn suggests a cooling of consumer demand and a potential "plateau" phase as the industry attempts to transition from early adopters to the broader mass market.

The State of the Market: A Year-over-Year Analysis

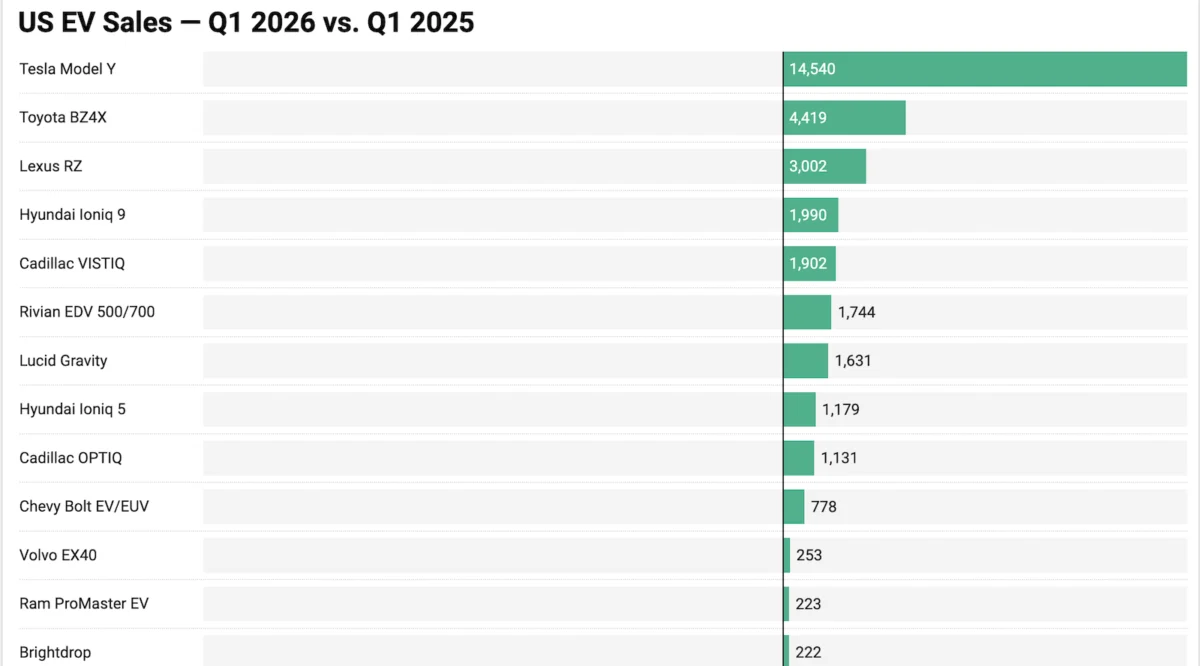

The shift in market dynamics is most evident when comparing Q1 2026 performance directly against the same period in 2025. The data reveals a volatile landscape where even established market leaders faced unprecedented headwinds. Tesla, which has long dominated the American EV space, presented a bifurcated performance. The Tesla Model Y emerged as the primary volume gainer, recording 14,540 more sales than it did in Q1 2025. However, analysts note that this growth is somewhat artificial; in early 2025, Model Y production lines were temporarily shuttered to facilitate a transition to a refreshed version of the vehicle. Consequently, the 2026 gains are measured against a suppressed baseline from the previous year.

Conversely, the Tesla Model 3 suffered the most significant volume loss in the industry. The electric sedan saw a decline of 20,848 units compared to Q1 2025, more than offsetting the gains made by its sibling, the Model Y. This decline is attributed to several factors, including increased competition in the sedan segment and a shift in consumer preference toward larger crossovers and SUVs.

Beyond Tesla, the market saw a surge from unexpected quarters. The Toyota bZ (formerly the bZ4X) and the Lexus RZ posted impressive growth, with volume increases of 4,419 and 3,002 units, respectively. This suggests that Toyota’s late-entry strategy into the battery-electric vehicle (BEV) space is beginning to gain traction among brand-loyal consumers. Other emerging models also showed promise, with the Hyundai IONIQ 9, Cadillac VISTIQ, Rivian EDV series, Lucid Gravity, and Cadillac OPTIQ all posting growth exceeding 1,000 units. It is important to note, however, that many of these models were either in early-stage launches or not yet available in Q1 2025, making their growth figures a reflection of new market entry rather than organic expansion of existing demand.

Strategic Retreats and Production Halts

The Q1 2026 data highlights a challenging period for traditional domestic and European automakers. Three prominent models—the Volkswagen ID.4, the Ford Mustang Mach-E, and the Honda Prologue—recorded substantial losses, with sales dropping by 7,325, 7,007, and 6,242 units, respectively.

The decline of the Volkswagen ID.4 has had immediate industrial consequences. Citing the cooling demand and the need to re-evaluate its North American electrification strategy, Volkswagen recently announced the cessation of ID.4 production in the United States. This move underscores the difficulties legacy manufacturers face in scaling EV production while maintaining profitability in a fluctuating market.

Ford’s performance also raised concerns among industry observers. The F-150 Lightning, once hailed as the vanguard of the electric truck revolution, has faced such significant headwinds that the company has moved toward discontinuing the current iteration. When comparing Q1 2026 to Q1 2024, Ford’s primary EV offerings—the Lightning and the Mustang Mach-E—each saw sales declines of several thousand units. This trend reflects broader struggles in the electric pickup segment, where high price points and towing-range concerns have slowed adoption among traditional truck buyers.

A Five-Year Chronology of the EV Market

To understand the Q1 2026 downturn, it is necessary to view it within the context of the last half-decade of EV adoption in the United States.

- 2021-2022: The Early Surge. During this period, the market was characterized by supply-side constraints rather than demand issues. EVs were often sold with significant dealer markups, and waiting lists stretched for months. In Q1 2022, the Tesla Model Y began its ascent toward becoming the best-selling vehicle globally.

- 2023: Scaling and Incentives. The implementation of the Inflation Reduction Act (IRA) provided a temporary boost to the market, though it also introduced complexities regarding battery sourcing and tax credit eligibility. By Q1 2023, several new models from Hyundai, Kia, and GM began to enter the fray.

- 2024: The Equilibrium Point. This year saw the first signs of a demand-supply rebalancing. Inventory levels at dealerships began to rise, and manufacturers started implementing aggressive price cuts to maintain volume.

- 2025: The Peak and Pivot. The third quarter of 2025 represented the high-water mark for EVs, reaching 10.6% of the total market. However, by the end of the year, high interest rates and a saturated early-adopter market began to weigh on sales.

- 2026: The Correction. The current data for Q1 2026 shows a market in a state of correction. The "chasm" between early adopters and the mass market has proven more difficult to cross than many executives predicted, leading to the 5.9% share currently observed.

Divergent Success Stories: General Motors and Toyota

Despite the general downturn, certain manufacturers have found success by targeting specific niches or price points. General Motors (GM) has seen a significant return on its Ultium platform investment with the Chevrolet Equinox EV. Comparing Q1 2026 to Q1 2024, the Equinox EV was the market’s largest winner, growing by 9,589 units. This success is largely attributed to its competitive pricing and its position as a viable electric replacement for the aging Chevrolet Bolt, which saw a decline of 6,249 units as it was phased out.

Toyota’s performance in Q1 2026 also offers a counter-narrative to the idea of a universal EV slowdown. The Toyota bZ grew by 8,132 units compared to two years ago. While Toyota has been criticized for its slow transition to full electrification, the recent surge suggests that its cautious approach—focusing on reliability and dealer network readiness—may be resonating with more conservative buyers who are now entering the EV market.

Economic and Infrastructural Implications

The contraction in EV market share in early 2026 is not occurring in a vacuum. Several external factors have contributed to the current environment:

- Interest Rates and Financing: Persistent high interest rates have made the total cost of ownership for new vehicles, which are often priced higher than their internal combustion engine (ICE) counterparts, prohibitive for many middle-income households.

- Charging Infrastructure Anxiety: Despite federal investments through the NEVI (National Electric Vehicle Infrastructure) program, the rollout of reliable high-speed charging stations has been slower than anticipated. Public perception of a "broken" charging network continues to be a primary deterrent for potential buyers.

- Residual Value Concerns: As manufacturers like Tesla have aggressively cut prices on new models, the resale value of used EVs has plummeted. This volatility has made leasing companies and individual consumers wary of the long-term financial implications of EV ownership.

Analysis of Future Implications

The Q1 2026 data suggests that the "inevitable" transition to electric mobility may be a longer and more non-linear process than previously forecast. For the industry to return to the 10% market share threshold, several shifts are likely required.

First, the industry must move beyond luxury and enthusiast models. The success of the Chevy Equinox EV indicates that there is significant pent-up demand for functional, affordable electric crossovers. Second, the discontinuation of models like the Ford F-150 Lightning and the VW ID.4 suggests a consolidation phase is underway. Automakers are likely to focus on fewer, more profitable models rather than attempting to electrify their entire portfolios simultaneously.

Furthermore, the "weirdness" of the Q1 2026 vs. Q1 2023 comparison—where many of today’s top sellers didn’t exist three years ago—highlights the rapid pace of product development. However, product availability alone is no longer sufficient to drive sales. The market has shifted from a "build it and they will come" phase to one that requires sophisticated consumer education, competitive financing, and a seamless charging experience.

While the drop to a 5.9% market share is a sobering statistic for proponents of clean transportation, the five-year view remains positive. Comparing Q1 2026 to Q1 2021, almost every manufacturer has seen a net gain in EV volume. The current downturn may represent a necessary cooling period that allows infrastructure to catch up with vehicle production, ultimately laying the groundwork for a more sustainable second wave of adoption in the late 2020s. For now, the US EV market remains a landscape of "winners and losers," where brand loyalty and price transparency are becoming the new metrics of success.

{kind=link}

Leave a Reply