The Volkswagen Group has released its financial and delivery results for the first quarter of 2026, revealing a complex landscape defined by resilient performance in Europe and significant headwinds in the United States and China. Despite a general contraction in the global automotive market and intensifying geopolitical tensions, the German conglomerate has maintained a stable global market share. Most notably, the company has doubled down on its commitment to Battery Electric Vehicles (BEVs), which featured prominently in the quarterly report, signaling a strategic divergence from several legacy competitors who have recently softened their electrification rhetoric.

Global Delivery Overview and Market Stability

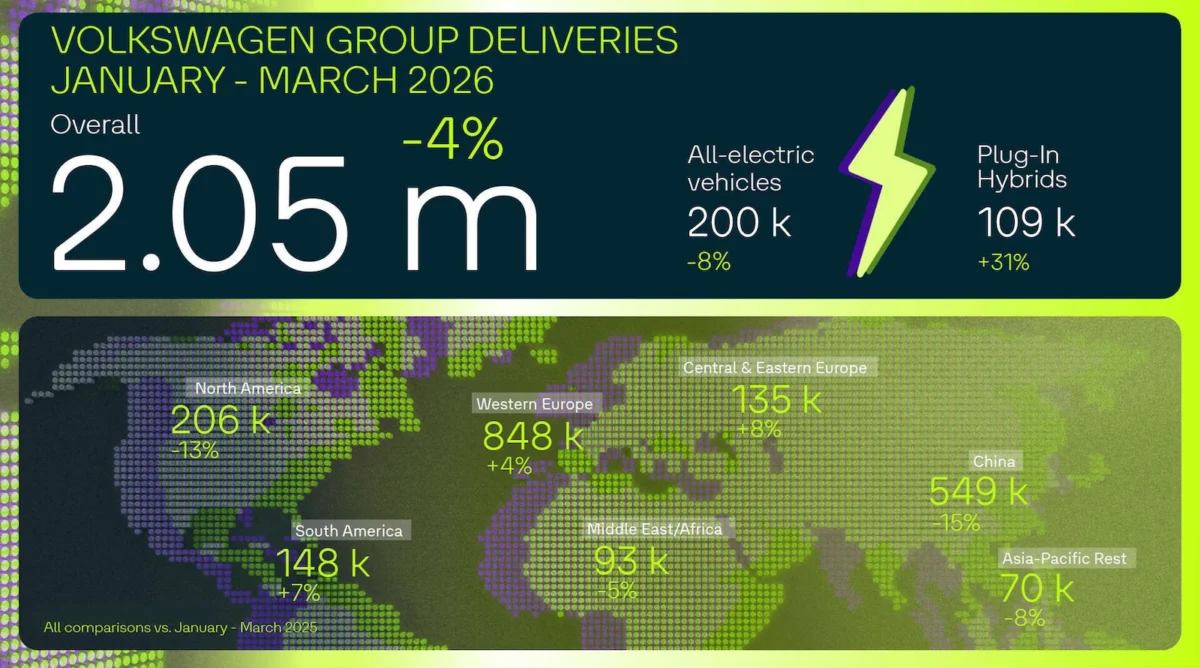

During the first three months of 2026, the Volkswagen Group navigated what executives described as "very challenging" economic conditions. High interest rates, fluctuating energy costs, and a general decline in consumer spending contributed to a cooling global automotive market. Nevertheless, Volkswagen reported that its overall delivery figures remained competitive, largely due to a robust performance in its home markets.

Marco Schubert, a member of the Group’s Extended Executive Committee for Sales, noted that while the worldwide market declined through the end of March, the Group’s ability to maintain market share was a testament to its brand diversity and regional adaptability. Schubert highlighted that the growth trend in Europe remained a primary engine for the company, even as other regions faced legislative and economic transitions. The report also addressed the ongoing conflict in the Middle East, stating that while disruptions occurred in directly affected localized markets, the impact on the Group’s global logistics and total deliveries remained statistically marginal.

European Leadership Amidst Regional Growth

Europe remains the cornerstone of Volkswagen’s electric transition. In the first quarter of 2026, the Group cemented its position as the clear BEV market leader on the continent. Deliveries of all-electric models in Europe rose by 12 percent year-over-year, a figure that stands in stark contrast to the declines seen in other major territories.

In Western Europe specifically, the BEV share of the Group’s total deliveries increased from 19 percent to 20 percent. This growth is attributed to a maturing charging infrastructure, continued institutional support for fleet electrification, and the popularity of the Group’s core electric lineup. Models from the Volkswagen, Audi, and Škoda brands have continued to perform well, with the company noting that European consumers are increasingly opting for electric mobility despite the removal of some direct purchase incentives in specific nations. This suggests that BEVs are reaching a point of organic demand in the European theater, independent of government subsidies.

Navigating Subsidy Expirations and Competitive Pressures in China

The situation in China, the world’s largest automotive market, presented a more difficult narrative for the first quarter of 2026. Volkswagen Group reported a significant 64 percent drop in BEV deliveries in the region. This decline is largely attributed to two factors: the expiration of major government subsidy programs at the end of 2025 and an aggressive price war initiated by domestic Chinese manufacturers.

The expiration of subsidies led to a "pull-forward" effect in late 2025, where consumers rushed to complete purchases before the price increase, leaving Q1 2026 with a depleted order bank. Furthermore, the Chinese market is currently in a state of high-velocity transition. Volkswagen is currently in the midst of a "In China, for China" strategy, which involves the development of local platforms and software tailored specifically to Chinese consumer preferences. The company indicated that the current dip is a transitional phase ahead of the launch of these new, locally developed electric models, which are expected to arrive in the latter half of the year to regain lost ground against local rivals like BYD and NIO.

The Impact of Trade Barriers on North American Operations

In the United States, the Volkswagen Group faced its steepest decline, with BEV deliveries falling by 80 percent compared to the same period in the previous year. This dramatic downturn is directly linked to the implementation of increased tariffs and revised trade policies that went into effect in April 2025. These measures have significantly altered the cost structure for imported electric vehicles and components, placing European manufacturers at a temporary disadvantage compared to domestically produced alternatives.

The U.S. market has also seen a cooling of BEV demand following the expiration of various federal and state-level tax credits. For Volkswagen, the 80 percent drop underscores the urgent need for localized production. The Group has been accelerating investments in its Chattanooga, Tennessee plant and exploring further North American manufacturing sites for battery cells and vehicle assembly to bypass the tariff barriers. Until these localized supply chains are fully operational, the Group expects continued volatility in its U.S. electric sales.

The Strategic Role of Second-Generation Plug-in Hybrids

While BEV growth faced regional hurdles, the Group’s Plug-in Hybrid Electric Vehicles (PHEVs) saw a substantial resurgence. Global PHEV deliveries reached 109,000 units in Q1 2026, representing an approximate 31 percent increase year-over-year.

This surge in demand is driven by the introduction of the Group’s "second-generation" PHEV powertrains. These modern systems offer significantly improved all-electric ranges—up to 143 kilometers (approximately 89 miles) on a single charge—allowing many commuters to operate entirely on electricity for daily use while retaining the flexibility of an internal combustion engine for longer journeys. This "bridge technology" has proven particularly popular in markets where charging infrastructure is still developing, or among consumers who remain hesitant to commit fully to a pure-electric platform. The success of the PHEV segment has provided a vital buffer for the Group’s overall fleet CO2 compliance.

Future Product Pipeline and the Electric Urban Car Family

Looking ahead, the Volkswagen Group is pinning its hopes for a Q3 and Q4 recovery on a flurry of new model launches. A central pillar of this strategy is the "Electric Urban Car Family" in Europe. These models, which include the production versions of the ID.2 and similar compact EVs from the Škoda and Cupra brands, are designed to bring the entry price of electric mobility down to the €25,000 mark.

The Group believes that these affordable, high-volume models will unlock a new segment of the market, particularly among younger buyers and urban dwellers. In China, the focus remains on the "New Energy Vehicle" (NEV) offensive, with models featuring enhanced connectivity and autonomous driving features developed in partnership with local tech firms. Schubert expressed confidence that these "key new models" would provide the momentum needed to offset the slow start to the year.

Top Performing Models and Brand Performance

Despite the regional fluctuations, several models maintained strong performance. The Group’s quarterly report highlighted its ten best-selling BEVs, which continue to be led by the Volkswagen ID.4 and ID.3, followed closely by the Audi Q4 e-tron and the Škoda Enyaq. The Porsche Taycan also remains a strong contributor to the Group’s margins, maintaining steady demand in the luxury segment.

The brand-specific data revealed that while the core Volkswagen passenger car brand felt the brunt of the China and U.S. slowdowns, premium brands like Audi and Porsche were somewhat more insulated due to their higher price points and more loyal customer bases. The commercial vehicles division also showed promise, with the ID. Buzz continuing to expand its footprint in both passenger and cargo configurations.

Analytical Outlook: Maintaining the Electric Momentum

The Q1 2026 results suggest that the transition to electric mobility is no longer a linear path but a fragmented regional journey. Volkswagen’s decision to keep BEVs at the forefront of its corporate communications—even when the data is unfavorable—marks a significant commitment to its "New Auto" strategy. By providing transparent context regarding the 80 percent drop in the U.S. and the 64 percent drop in China, the Group is attempting to reassure investors that these are external, policy-driven setbacks rather than a failure of the product itself.

The 12 percent growth in Europe is the "proof of concept" that the Group needs to justify its long-term investments. If Volkswagen can replicate its European market share stability in the U.S. and China through localized production and more affordable models, it remains well-positioned to dominate the latter half of the decade. However, the short-term challenge remains the navigation of protectionist trade policies and the aggressive pricing strategies of competitors in the Asian market.

As the Group moves into the second quarter of 2026, the focus will shift toward scaling battery production at its PowerCo subsidiaries and ensuring the software integration for its next-generation platforms is seamless. The rise of PHEVs suggests a more pragmatic consumer base than previously anticipated, and Volkswagen’s ability to pivot between pure electrics and high-range hybrids may be its greatest competitive advantage in a volatile global economy.

In conclusion, while the first quarter of 2026 was marked by significant contraction in key markets outside of Europe, the Volkswagen Group’s maintained market share and surging hybrid sales indicate a resilient business model. The company’s transparency and continued focus on its electrification roadmap suggest that it views the current geopolitical and economic disruptions as temporary hurdles on an inevitable path toward a decarbonized automotive future.

{kind=link}

Leave a Reply